Atradius Atrium

Get direct access to your policy information, credit limit application tools and insights.

Australia

Australia

Austria

Austria

Belgium

Belgium

Brazil

Brazil

Bulgaria

Bulgaria

Canada

Canada

China

China

Czech Republic

Czech Republic

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Greece

Greece

Hong Kong SAR

Hong Kong SAR

Hungary

Hungary

India

India

Ireland

Ireland

Italy

Italy

Japan

Japan

Lithuania

Lithuania

Mexico

Mexico

Netherlands

Netherlands

New Zealand

New Zealand

Norway

Norway

Poland

Poland

Portugal

Portugal

Romania

Romania

Singapore

Singapore

Slovakia

Slovakia

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

Turkey

Turkey

United Arab Emirates

United Arab Emirates

United Kingdom

United Kingdom

United States

United States

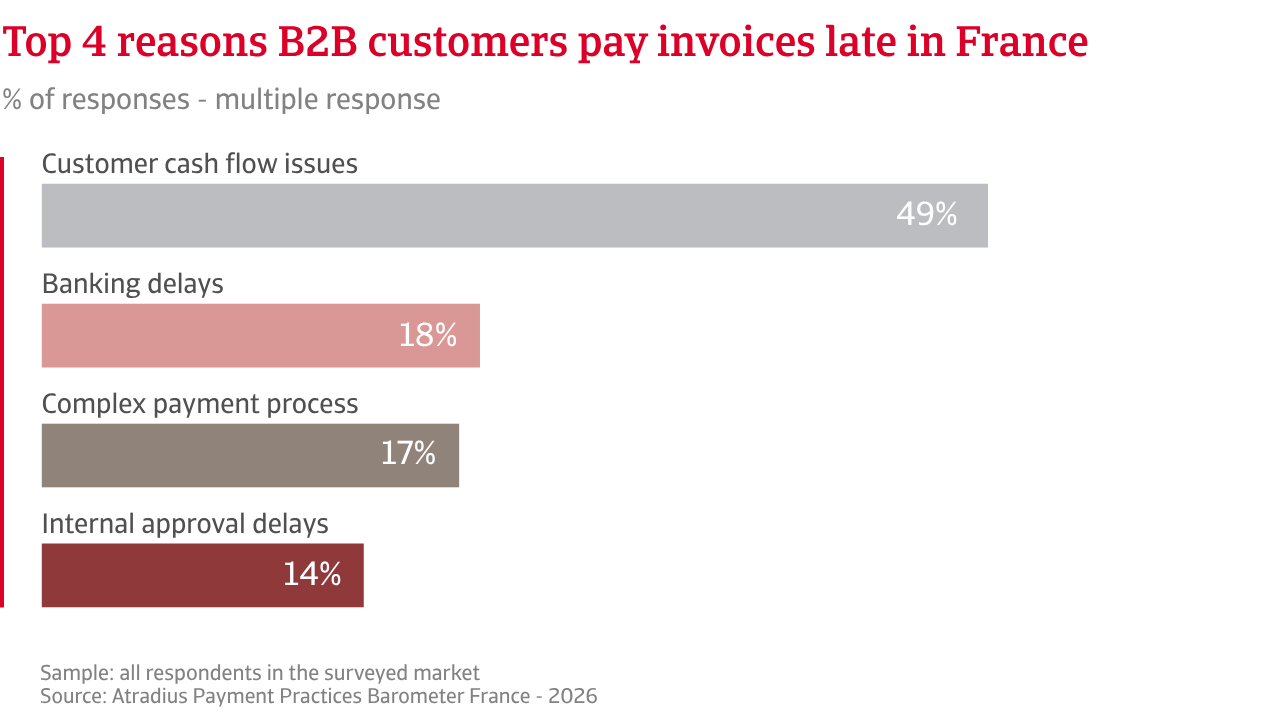

The escalation of geopolitical turmoil in the Middle East is weighing on customer liquidity across Western Europe, adding pressure to business-to-business (B2B) payment patterns. This helps explain why nearly half of French businesses have reduced selling on credit in B2B trade, limiting reliance on this commercial tool to just 22% of B2B sales, around thirty percentage points below the regional average. Where supplier credit is used, it is mainly concentrated among trade focused SMEs, for which selling on credit helps secure orders in highly competitive markets with limited pricing flexibility.

Fewer businesses in France set payment terms within the 30-day window commonly used across Western Europe, while terms of up to two months from invoicing are more prevalent. Rather than signalling confidence in customer payment reliability, this shift toward more flexible terms reflects a defensive response by suppliers to deteriorating customer payment behaviour from B2B customers, driven mainly by customer liquidity stress.

Against this backdrop, late payment now affects around three in five French businesses. This share sits above the regional average, while the share of delayed invoices in France remains lower than across Western Europe overall, reflecting the more limited use of supplier credit in French B2B trade. Once overdue, invoices are paid on average just over three weeks past due, broadly in line with the regional timing. The lower reliance on trade credit in France limits the share of invoices entering extended payment periods. This pulls average Days Sales Outstanding (DSO) down and constrains the build-up of long aged receivables.

Across Western Europe, by contrast, broader use of trade credit and earlier entry into overdue status push a larger share of invoices into longer ageing buckets, increasing exposure to bad debt and write offs. More than four in five French businesses limit bad debt below 1% of B2B invoices, compared with a lower share of companies across Western Europe, where losses are more widely distributed at higher levels. Working capital pressure affects companies in both France and the region, but its expression differs.

In France, companies show a stronger preference for preventive and structural measures, including requesting upfront payment terms and reserve building. Across Western Europe there is greater emphasis on active intervention once risk has emerged, with wider use of credit monitoring, collections, and automated processes. Credit insurance remains a core tool in both markets, used by around one quarter of businesses, signaling a shared foundation in formal risk transfer.

Nearly half of French businesses have reduced selling on credit in B2B trade, limiting reliance on this commercial tool to just 22% of B2B sales, around thirty percentage points below the regional average.

Amid widespread uncertainty over the evolution and duration of the geopolitical turmoil in the Middle East, risks remain elevated, adding to downside pressures on the French economy. Higher inflation, a weaker trade environment, tighter financial conditions, and the erosion of business sentiment create negative feedback within the domestic market.

Against this backdrop, expectations around B2B customer payment behaviour remain weak in France, reinforcing the cautious stance many suppliers have adopted toward granting trade credit. More French businesses expect payment behaviour to deteriorate rather than improve in the short term, in contrast with Western Europe, where expectations are more balanced. This divergence reflects persistent liquidity stress among customers and helps explain why French suppliers remain reluctant to expand credit exposure, despite competitive pressure.

Concern extends beyond payment delays to customer solvency. Close to four in ten French businesses expect insolvency levels to rise over the coming year, compared with just under three in ten across Western Europe. While a slim majority in both markets do not anticipate an increase, the higher share of pessimistic businesses in France points to deeper concern about customer financial health. Fewer French firms report uncertainty, suggesting expectations are more firmly anchored rather than provisional.

Margin expectations add another constraint. Profit outlooks remain fragile in France, contrasting with Western Europe where sentiment is more constructive. Continued cost pressure, limited pricing power, and subdued demand weigh on profitability. Thin margins leave little room to absorb payment shocks, reinforcing a preference for tighter credit discipline and cash protection. Broader risk perceptions further strengthen this stance.

A clouded economic outlook stands out as the dominant perceived risk to B2B payment behaviour in both France and Western Europe, but concern is notably stronger in France. This signals heightened anxiety about unpredictable customer liquidity shifts in the short term. Sector specific downturns also feature more prominently in France than across the region, suggesting stress is increasingly concentrated in exposed industries.

Taken together, weak payment outlooks, expectations of rising insolvency levels, and more fragile profit margins underpin a conservative approach to trade credit in France. Credit is extended selectively and defensively, managed as exposure to be contained rather than a lever for growth. A broad loosening of trade credit conditions in France appears unlikely over the coming months, given heightened risk concerns around the short-term outlook for B2B payment behaviour.

For a full overview of the 2026 survey results for France and Western Europe, please download the market specific report from the related documents section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.