Atradius Atrium

Get direct access to your policy information, credit limit application tools and insights.

Australia

Australia

Austria

Austria

Belgium

Belgium

Brazil

Brazil

Bulgaria

Bulgaria

Canada

Canada

China

China

Czech Republic

Czech Republic

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Greece

Greece

Hong Kong SAR

Hong Kong SAR

Hungary

Hungary

India

India

Ireland

Ireland

Italy

Italy

Japan

Japan

Lithuania

Lithuania

Mexico

Mexico

Netherlands

Netherlands

New Zealand

New Zealand

Norway

Norway

Poland

Poland

Portugal

Portugal

Romania

Romania

Singapore

Singapore

Slovakia

Slovakia

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

Turkey

Turkey

United Arab Emirates

United Arab Emirates

United Kingdom

United Kingdom

United States

United States

Companies in Hungary continue to rely on trade credit, though with a measured approach. Nearly half of all business-to-business (B2B) sales are made on credit. This sits slightly above the Central and Eastern Europe (CEE) average and is led by medium and large service firms.

Credit use is rising across CEE despite a preference for cash sales, although Hungary is expanding more gradually than the region. This reflects a clear balancing act between supporting sales growth and safeguarding liquidity. That caution is reflected in B2B payment terms, with Hungarian firms preferring shorter due dates. More businesses in Hungary than in CEE set payment deadlines within 30 days from invoicing. Longer terms remain limited, mostly among small construction firms.

Late payment remains widespread. 78% of Hungarian companies report overdue invoices, only slightly below the regional average. The key difference lies in exposure. Hungarian firms carry a lower share of overdue receivables, indicating more contained risk. Settlement timings further support this view. Payments are recovered more quickly than in the region. Delays extending well beyond due dates are less frequent, although the longest delays remain comparable to peers. Over three quarters of businesses report that overdue invoices being settled within one month beyond the due date. This limits the build-up of late payments and contains Days Sales Outstanding (DSO) volatility.

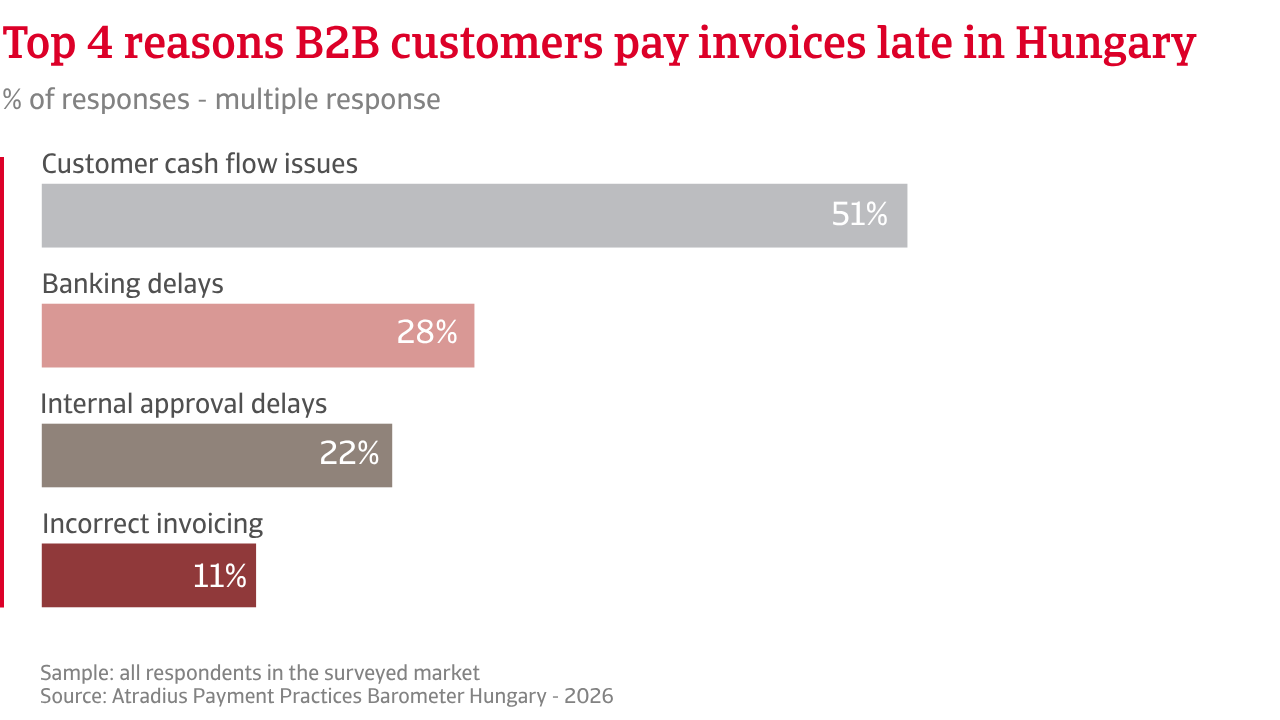

The drivers of delay also differ between Hungary and CEE. Liquidity stress is less often cited. Instead, companies highlight banking processes and internal approval bottlenecks. Operational inefficiencies play a larger role than financial distress. Addressing these frictions could unlock faster payments.

Bad debt levels remain comparatively low. More Hungarian firms report minimal write-offs than in the region. Decisions are mainly driven by the age of receivables and customer insolvencies, in line with regional practice.

Hungary’s macroeconomic environment provides a cautious backdrop for B2B payment behaviour. After a period of weak growth, the economy is entering a modest recovery, with inflation continuing to weigh on costs and liquidity. For businesses, this means ongoing pressure on margins and a measured approach to trade credit, with firms remaining cautious in extending payment terms and closely managing working capital.

The impact on working capital is more contained in Hungary than in CEE. Fewer firms report liquidity strain, reduced cash buffers or reliance on external finance. Operational stress is also limited, with less need to delay supplier payments or cut investment.

Risk management reflects these conditions. Hungarian firms rely less on reactive measures such as shortening terms or legal action. Instead, they focus on structural tools, including digital payments and customer diversification. Overall, Hungary presents a stable payment environment, with lower but firmly persistent credit risk.

Nearly half of all business-to-business (B2B) sales are made on credit. This sits slightly above the CEE average and is led by medium and large service firms.

Across business segments, companies in Hungary expect little short-term change in the payment behaviour of business customers. Expectations remain balanced between improvement and deterioration, reflecting ongoing economic uncertainty and mixed sector performance. The outlook remains stable, with no clear evidence of recovery taking hold. This contrasts with the broader CEE region, where expectations are more varied. Some markets show growing confidence, while others remain constrained by weak economic conditions. The regional picture shows mixed recovery paths rather than a single clear trend.

Insolvency expectations further underline this gap. In Hungary, around 43% of businesses expect insolvency risk to rise, while a similar share anticipate it will remain high. This points to stability rather than increase. Businesses continue to face persistent financial pressure, with limited hope of short-term easing. Across CEE, businesses take a more cautious view, expecting insolvencies to increase, highlighting a more uncertain and weaker outlook. Compared with Hungary, the regional picture is more tilted towards downside risk.

Turning to profitability expectations, Hungarian businesses show limited confidence in achieving short term margin growth, while responses from companies across CEE are slightly more positive, highlighting uneven confidence and economic conditions across markets. These views translate into payment risk, as weaker margins in Hungary have the potential to limit cash flow and increase the risk of delays or defaults, while stronger expectations in CEE help only slightly, as the overall payment risk environment remains weak.

When asked about the top risks that could disrupt B2B payment behaviour in the coming months, four in five businesses in Hungary, well above the regional average, point to the macroeconomic environment, particularly the risk of an economic slowdown. Inflation and cost pressures on the business follow closely, cited by two thirds of firms. Together, these factors contribute to ongoing pressure on demand, margins, and overall business resilience. Currency volatility and interest rates matter, but do not reach critical levels. Operational risks, including supply chain disruption and fraud, are less prominent than in CEE. The focus remains firmly on core economic constraints.

Across the region, the picture is very similar but more widespread, with businesses also highlighting economic slowdown and inflation as key risks, though at lower levels. This suggests that businesses in Hungary feel more vulnerable to macroeconomic shocks, with greater potential strain on payment behaviour and financial resilience than peers across CEE.

For a full overview of the 2026 survey results for Hungary, please download the market specific report from the related documents section below. Insights into Central and Eastern Europe (CEE) are available in the related content section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.