Atradius Atrium

Get direct access to your policy information, credit limit application tools and insights.

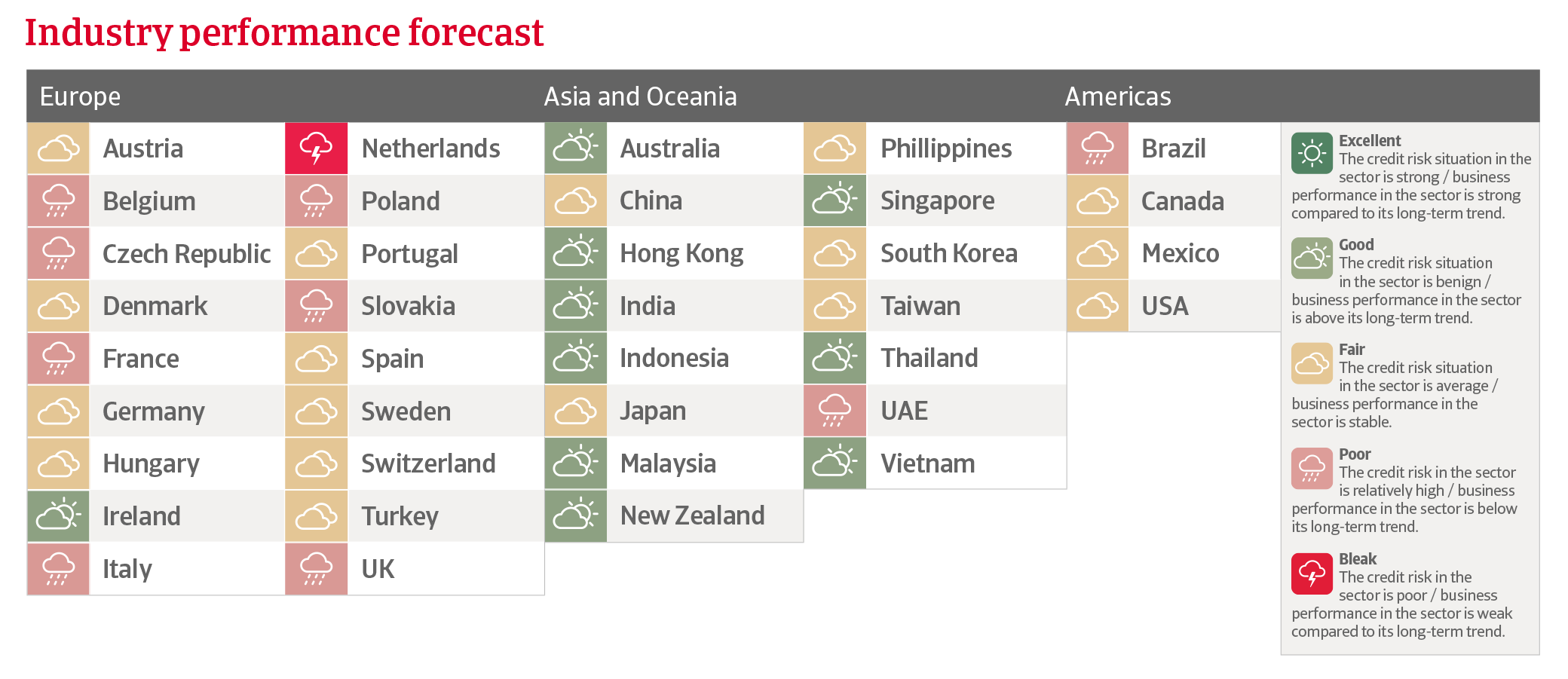

Australia

Australia

Austria

Austria

Belgium

Belgium

Brazil

Brazil

Bulgaria

Bulgaria

Canada

Canada

China

China

Czech Republic

Czech Republic

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Greece

Greece

Hong Kong SAR

Hong Kong SAR

Hungary

Hungary

India

India

Ireland

Ireland

Italy

Italy

Japan

Japan

Lithuania

Lithuania

Mexico

Mexico

Netherlands

Netherlands

New Zealand

New Zealand

Norway

Norway

Poland

Poland

Portugal

Portugal

Romania

Romania

Singapore

Singapore

Slovakia

Slovakia

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

Turkey

Turkey

United Arab Emirates

United Arab Emirates

United Kingdom

United Kingdom

United States

United States

Provided that the war is temporary, and the Strait of Hormuz gradually reopens from May, based on an Oxford Economics assessment we expect global chemicals production to increase by 0.6% in 2026, 1.6 percentage points lower compared with pre war expectations.

In a downside scenario where we see a prolonged conflict and a closure of the Strait into September, global chemicals production would shrink 1.7%, with the contraction in the eurozone accelerating to 4.3%. As a result of elevated exposure to the Gulf supply shock, Asian chemicals output would contract by 0.6% in 2026.

Chemicals companies are facing renewed uncertainty surrounding tariff regimes and legal risks. A key concern remains the potential diversion of Chinese goods - originally destined for the US - into other markets, particularly Europe. This shift could lead to an influx of cheaper Chinese products, undercutting demand for domestically manufactured goods.

The chemicals industry is characterised by intense competition and ongoing market consolidation. Larger players often have economies of scale and greater resources to invest in research and development, innovation and marketing. This may cause smaller companies to struggle to remain competitive.

We expect US chemicals sector production to mildly decrease by 0.5% in 2026. Headline output is being weighed down by the soaps, polish and detergent subsector, where production is expected to fall by almost 3%.

US industrial production growth of 1.4% should support chemicals demand from manufacturers, but there are downside risks: US automotive production as a key downstream sector is expected to contract by 2.5% this year. A near-term pullback in consumer spending, increased uncertainty due to the Gulf war and tariff policy changes could also negatively impact chemicals demand.

On the positive side, the US chemicals sector is somewhat shielded from shocks to global energy prices. Investments in US shale gas-related projects over the past decade have been large, resulting in more stable gas prices. This is helping US chemicals producers to enjoy an advantage in cost competitiveness over their European and Asian peers.

We expect US chemicals production to rebound by 2.5% in 2027, supported by a robust 2.7% economic growth rate. The US administration’s expansionary fiscal policy lifts household spending and business investment, boosting demand for manufactured and chemical goods.

After strong increases in 2024 and 2025, China’s chemical production growth is expected to slow to 2.7% in 2026 and 3.0% in 2027. The country’s economy and industry have been relatively resilient to the global energy crunch so far.

However, this resilience does not mean that the economy is immune to softer external demand and tighter global financial conditions. Those will negatively impact demand for Chinese exports, including chemicals.

Given the oversupply of housing, construction volumes will remain low, reducing demand for chemical goods from a key downstream sector. China has a significant overcapacity issue, impacting margins for many Chinese chemicals producers.

In international comparisons Chinese chemicals production remains competitively priced, supporting exports. The sector is a strategic priority for the Chinese authorities, and we expect ongoing fiscal support to offset any potential trade losses.

We expect Japan’s chemicals output to contract by 4.8% in 2026, followed by a 0.7% decline in 2027. Producers in Japan rely heavily on oil from the Middle East (around 95% of its oil supply coming from the region). Some businesses have already started to cut production because of the dwindling feedstock supply.

Demand from key buyer sectors like automotive and construction is subdued. Additionally, US tariffs and overcapacity weigh on growth.

Japanese basic chemicals producers feel competitive pressure from their cheaper producing Chinese and US peers. Growing Chinese oversupply remains a key challenge for the sector and is forcing Japanese producers to rationalise production.

The European chemicals industry is heavily affected by the sharp rise of oil and gas prices due to the Gulf war, which makes feedstock and energy used to create chemicals even more expensive.

There is higher credit risk for smaller European chemicals producers without energy hedging, while larger players focusing on speciality chemicals still perform quite well.

The repeated surge in European gas prices is worsening long standing competitiveness issues, particularly relative to China and the US. In addition to these energy related challenges, European chemicals firms face growing pressure to invest in automation, transformation and digitalisation.

Consequently, we expect chemicals production in the EU and the UK to decrease by 2.2% in 2026, 1.8 percentage points more than the pre-war forecast in February. We have recently downgraded our business performance/credit risk outlook for the chemicals industry in Belgium, Italy, the Netherlands and the UK.

In order to cut costs and to improve operational efficiency, several facilities have been closed over the past two years in the EU and the UK. We expect an orderly but significant consolidation process in the coming years.

SMEs without energy hedging and without the investment power for decarbonisation are particularly at risk, while large, efficient players focusing on speciality chemicals enjoy a competitive advantage.

Germany´s chemical sector is forecast to suffer a 4.7% output contraction this year. The industry is facing a combination of high energy prices, weak domestic and European demand, US tariffs and increasing global competition.

Several chemicals manufacturers have already relocated to countries where energy costs are lower. High costs, regulatory requirements, and global trade shifts are increasingly influencing investment decisions.

Credit risk has increased for basic chemicals SMEs without pricing power, as well as for smaller businesses without energy hedging and lack of funding for investment in decarbonisation.

Also vulnerable are companies with high dependency on gas and suppliers affected by tariffs. Banks are now taking a much more critical look at refinancing in the chemicals sector, and financing partners are significantly less involved..

That said, performance of speciality chemicals remains more robust, a segment in which German producers have high expertise. Additionally, demand is rising for chemicals in sustainability-focused sectors, including electric vehicles, as well as life sciences.

Download the full report in the related documents section below for a detailed analysis of the challenges, performance, and credit risks facing the chemicals industry’s major markets throughout the world.

To explore to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.