Atradius Atrium

Get direct access to your policy information, credit limit application tools and insights.

Australia

Australia

Austria

Austria

Belgium

Belgium

Brazil

Brazil

Bulgaria

Bulgaria

Canada

Canada

China

China

Czech Republic

Czech Republic

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Greece

Greece

Hong Kong SAR

Hong Kong SAR

Hungary

Hungary

India

India

Ireland

Ireland

Italy

Italy

Japan

Japan

Lithuania

Lithuania

Mexico

Mexico

Netherlands

Netherlands

New Zealand

New Zealand

Norway

Norway

Poland

Poland

Portugal

Portugal

Romania

Romania

Singapore

Singapore

Slovakia

Slovakia

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

Turkey

Turkey

United Arab Emirates

United Arab Emirates

United Kingdom

United Kingdom

United States

United States

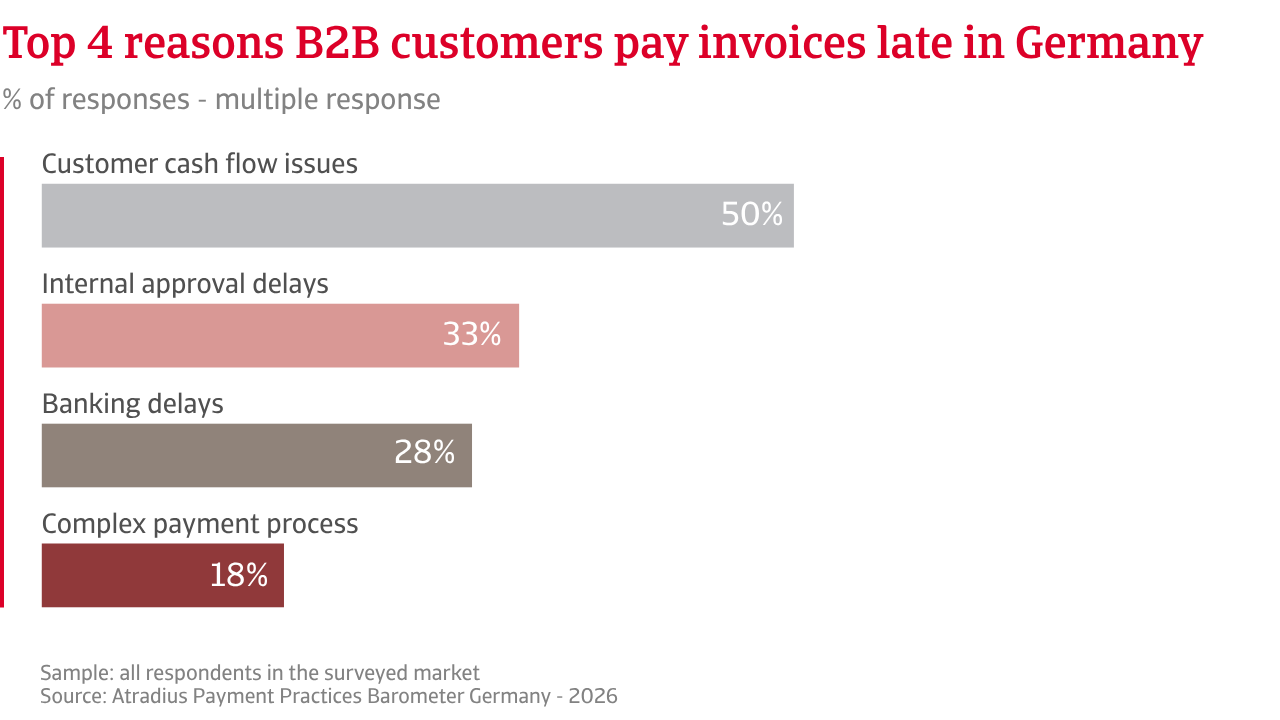

Bank lending conditions have tightened across Western Europe in the past few years, driven by higher perceived credit risk. Germany feels this pressure more acutely, as its businesses rely heavily on bank financing. As bank credit becomes harder to access, companies struggle to secure funding for working capital and day-to-day operations. As a result, businesses turn to alternative sources of short-term financing. Supplier credit has expanded as the main substitute for bank loans and now plays a more central role in corporate finance in Germany.

Most German companies selling on credit in business-to-business (B2B) trade offer payment terms within a 30-day window, reflecting the pattern seen across Western Europe. Longer terms of up to two months or more are far less common. Suppliers in Germany remain more risk averse and prioritise protecting their own liquidity. This limits customers’ ability to ease cash flow pressures, reflecting a cautious approach to credit risk in German B2B trade. This approach also means fewer suppliers in Germany than in Western Europe offer trade credit in B2B sales. About 52% of B2B sales are made on credit across the region, while in Germany the figure falls to just 35%. Buyers must therefore deploy their own cash earlier, increasing pressure on working capital and weakening liquidity positions.

This has driven a clear deterioration in customer payment behaviour. Late payments are now more widespread in Germany than across Western Europe, with 87% of German companies reporting B2B delays, compared with 77% regionally. Longer cash conversion cycles have pushed Days Sales Outstanding higher across several sectors, undermining reliable cash flow planning. As liquidity stress intensifies, vulnerability to insolvency risk increases. This may explain the increase in bad debts across multiple sectors in Germany, with SMEs and highly leveraged firms remaining particularly exposed. Many more companies in Germany than regionally report bad debts clustered around 5% of total B2B invoices. At this level, bad debts steadily erode working capital and weigh on business profitability.

Survey data reveal contrasting approaches to payment risk management in Germany compared with Western Europe. German businesses show stronger reliance on internal credit controls, more often absorbing risk internally through active credit management, automated collections, and loss provisions. Western European firms more frequently limit risk at the point of sale through upfront or partial payments, protecting liquidity at an earlier stage. Slightly below the regional average, around one in four German companies surveyed report using credit insurance. They view it as a complement to internal credit controls, transferring part of the loss risk externally. When late payments rise and economic uncertainty increases, and suppliers absorb most of the risk, credit insurance helps make this model more resilient.

Suppliers in Germany remain more risk averse and prioritise protecting their own liquidity. This means fewer suppliers in Germany than in Western Europe offer trade credit in B2B sales.

As late payments are now more widespread in Germany than across Western Europe, businesses show little confidence in a short-term improvement in B2B payment behaviour. Pessimism is strongest among German manufacturers and trading companies. Many expect the liquidity squeeze to intensify in the coming months. Ongoing geopolitical tensions, including sudden trade policy shifts and conflicts, add another layer of uncertainty, especially for export-exposed firms.

Against this backdrop, customer payment risk is expected to remain elevated across both Germany and Western Europe, with no clear signs that the pace of deterioration is easing. Germany faces significant strain, as high insolvency levels continue to weigh on the business environment. Concern over a further rise in company failures in the short term intensifies pressure along supply chains. This would reduce the ability of weaker firms to absorb late payments, reinforcing the need for tighter cash management. German companies remain pessimistic about short term profitability, with sentiment lagging behind Western Europe. Economic and trade uncertainty continues to limit scope for margin recovery, even as demand shows tentative signs of stabilising. Slightly stronger optimism across western Europe suggests firms there feel better positioned to protect margins under current conditions.

The risk landscape in Germany broadly mirrors that in Western Europe but appears more acute across several dimensions. Heightened geopolitical uncertainty and higher energy prices are set to push inflation higher this year. This weighs on real incomes and weakens purchasing power. This may explain why economic contraction is the dominant concern for more than three-quarters of German businesses, a higher share than the regional average. Downside risks have increased further. Rising energy costs and ongoing uncertainty linked to the conflict in the Middle East threaten Germany's already fragile growth prospects, particularly if energy prices remain elevated for longer.

Sector specific risks pose a significant downside to the German economy. Global trade unpredictability affects German firms more severely due to their deep exposure to international markets and complex supply chains. This amplifies vulnerability to external shocks and disrupts revenue visibility. At the same time, macroeconomic weakness, persistent cost pressures, and rising insolvencies compress liquidity buffers, further restricting financial flexibility. Together, these factors intensify liquidity stress and reduce firms’ capacity to absorb additional shocks, increasing reliance on disciplined cash management and active payment risk mitigation.

For a full overview of the 2026 survey results for Germany and Western Europe, please download the market specific report from the related documents section below.

To explore how to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.