Atradius Atrium

Get direct access to your policy information, credit limit application tools and insights.

Australia

Australia

Austria

Austria

Belgium

Belgium

Brazil

Brazil

Bulgaria

Bulgaria

Canada

Canada

China

China

Czech Republic

Czech Republic

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Greece

Greece

Hong Kong SAR

Hong Kong SAR

Hungary

Hungary

India

India

Ireland

Ireland

Italy

Italy

Japan

Japan

Lithuania

Lithuania

Mexico

Mexico

Netherlands

Netherlands

New Zealand

New Zealand

Norway

Norway

Poland

Poland

Portugal

Portugal

Romania

Romania

Singapore

Singapore

Slovakia

Slovakia

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

Turkey

Turkey

United Arab Emirates

United Arab Emirates

United Kingdom

United Kingdom

United States

United States

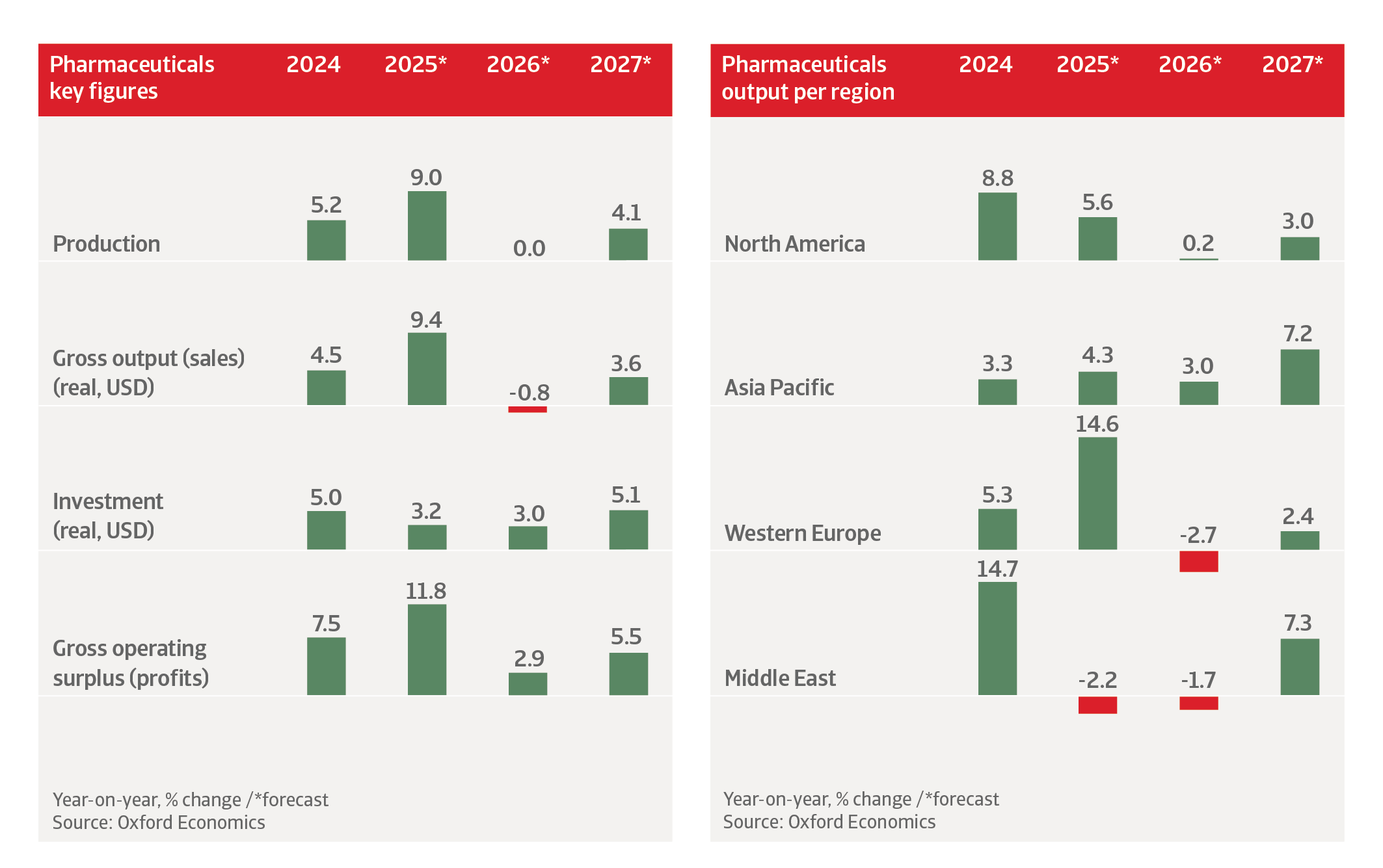

Global pharmaceutical production increased by 9.0% in 2025, mainly due to front-loading activity in anticipation of US tariffs. In 2026 output growth is expected to level off, as a retrenchment following last year’s surge has dampened production in H1 of 2026. Additionally, the Gulf conflict has an impact, although mostly indirect. The Middle East itself produces only a small share of global pharmaceutical ingredients (about 0.5%) but increases in oil and gas prices have raised manufacturing and transportation costs for pharmaceuticals. Cold-chain logistics, APIs, packaging, and air freight remain vulnerable to any prolonged disruption. Recent developments suggest the conflict may be entering a fragile de-escalation phase, with a reopening of the Strait of Hormuz. However, in case of another flare-up of the conflict with the closing of the Strait continuing until the end of the year and beyond, pharmaceutical growth would contract by 0.8% in 2026 and grow just 2.3% in 2027.

The impact of recent US tariffs remains limited, as they only apply to patented drugs. The US has granted exemptions to most major pharmaceutical producers and most trading partners have received a preferential rate. However, the downside risk of another tariff flare-up remains.

In the coming years industrial policy will play a larger role throughout the global pharmaceuticals product value chain. The Covid-19 pandemic and geopolitical tensions have exposed vulnerabilities in national health systems, e.g. heavy reliance on imported active pharmaceutical ingredients (APIs). This has resulted in a series of actions like the EU Critical Medicines Act to reduce reliance on imports, and to incentivise local investments and strategic stockpiling. As a consequence we expect a reconfiguration of pharmaceuticals and medical devices supply chains in the future.

In general, the industry has robust equity, solvency and liquidity. Most pharmaceuticals and biotech businesses enjoy good access to external financing to help sustain high R&D costs. However, the industry (in particular big pharma businesses) is confronted with a major patent cliff that will continue through to 2030, with top-selling oncology, immunology, and metabolic drugs facing the loss of exclusivity over the next few years.

Globally there is a shift towards premium and differentiated pharmaceutical products, including biologics, antibody-drug conjugates, and cell and gene therapies. Demand for GLP-1 weight-loss drugs remains strong, and producers of medication in this segment are facing growth predictions of about USD 80 billion by 2030. We expect that Artificial Intelligence (AI) will increase productivity in the pharmaceutical sector in the coming years, mainly by supporting the preclinical phase and R&D in the production pipeline.

In the mid and long-term, the developed world will remain a major source of demand for pharmaceuticals, as ageing and increasingly overweight populations drive demand for high value-added speciality products aimed at chronic diseases as well as generic drugs. In emerging markets, rising insurance coverage, diagnostics uptake, and treatment of chronic disease support structurally strong demand. However, longer-term expansion could be restrained as governments push for cost control and introduce drug price negotiations. Healthcare spending cuts could affect R&D investment given the high cost of developing new drugs.

We expect US pharmaceuticals output growth to decelerate to 0.1% in 2026 after a strong 6.3% increase in 2025. The unwinding of frontloading in anticipation of tariffs, pricing pressure and softer healthcare spending is impacting output growth despite the strong demand for GLP-1 treatments and biologics. In 2027 a 3.2% rebound is forecast.

In early April 2026 the US administration announced that pharmaceutical tariffs of up to 100% under Section 232 would go into effect as soon as July 31. However, the tariffs only apply to patented drugs and not generics. Affected pharmaceutical imports will likely see a wave of order frontloading before the tariffs are implemented – though the impact is likely to be minor. A lower 15% tariff rate will be placed on drugs from the EU, Japan, Korea, and Switzerland. We assume that more than a dozen of the largest global pharmaceutical companies will end up fully exempted from tariffs, as they agreed to sell certain drugs and future medicines at lower prices under a so-called “most favoured nation” framework. As part of the agreements, they have also pledged to invest heavily in the US, expanding their R&D and manufacturing capacity. Given all the carveouts, the pharmaceutical tariffs are estimated to add only 0.8 percentage points to the overall US effective tariff rate.

It is expected that the Trump administration will decrease regulatory hurdles for domestic facility construction in order to incentivise reshoring to the US. This could further boost pharmaceuticals production in the US. However, high production costs could still make it more cost-effective for pharmaceuticals to be manufactured elsewhere.

Demand for pharmaceuticals will be driven by the ageing population in the US. Companies making speciality products, like medicines for chronic conditions and generic drugs, will find growth opportunities here. A surge in demand for weight-loss drugs will also benefit the US pharmaceuticals market in the coming years. That said, currently only half of obese Americans have access to the drugs through their health insurance.

The strong financial footing of US pharma businesses could come under increasing pressure from structural changes.

Margins for branded pharmaceuticals are robust, leading to strong cash flow and credit profiles. Many US pharmaceutical companies seem financially strong or have ample liquidity sources in the financial markets. However, this strong financial footing could come under increasing pressure from structural changes in the competitive and regulatory environment.

While patented drugs will continue to dominate the market, there is growing competition as both generics and biosimilars increase their market share, driven by the loss of patent protections on established drugs. According to the US Food and Drug Administration (FDA), more than 75 biosimilars were approved in 2025, expanding competitive pressure in several biologics-heavy therapy areas. Recent regulatory changes, including streamlined guidance on interchangeability, are lowering practical barriers to biosimilar adoption and strengthening price competition for off-patent biologics. Approval rates of generic drugs also remain high, further intensifying the competitive landscape. At the same time, the US government has taken steps to reduce the price of pharmaceuticals for consumers, which could erode businesses’ margins. Overall, the industry is objecting to these measures, arguing that they could lower innovation as businesses become discouraged to invest in R&D if returns on their investments are uncertain.

We expect production of Chinese pharmaceuticals to grow by 5.1% in 2026 and by 6.2% in 2027. The sector’s short- and mid-term outlook remains benign. Tariff exposure to the US is limited, as pharmaceutical exports to the US account for only 2% of nominal gross output. China accounts for about 40% of global active pharmaceutical ingredients (API) output, but those are not targeted by US tariffs.

The government has been successful in making the country attractive for pharmaceutical production and innovation, shifting away from producing generics and towards high quality drugs and biopharmaceutical innovations. Measures include a series of capital investments, support of R&D, and policies designed to streamline approval processes and to align regulations with international standards. However, the sharp increase in pharmaceuticals output has also increased safety concerns about production standards, attracting more scrutiny by regulatory authorities.

China has been successful in shifting away from producing generics and towards high quality drugs and biopharmaceuticals.

Biologics and innovative drugs now account for roughly 40% of China’s development pipelines, with China contributing around 30% of global clinical trials (up from 5% ten years ago). Novel medicines are becoming the main growth engines, with domestic champions continuing to report strong innovation-drug revenue growth, even as legacy generic margins contract. There is policy support to attract foreign investment in cell and gene therapy, with a designated zone in Pudong, Shanghai, that aspires to become a global hub for gene therapy innovation, clinical testing, and manufacturing. In the first half of 2025 about a third of all global licensing agreements signed by large multinational pharma firms were with Chinese businesses. These partnerships reflect confidence in the country’s biopharmaceutical ecosystem.

The domestic market is highly price sensitive, as public procurement continues to suppress prices of mature drugs. In China most sales are still of generic drugs. State insurance covers most purchases, pooling demand from hospitals. In order to obtain coverage, producers have to lower prices to reach a large patient pool. The state’s volume-based procurement (VBP) programme is covering over 400 medicines cumulatively and driving average price cuts of 40%–60% on off-patent drugs, accelerating consolidation among small generic manufacturers.

Mid- and long-term domestic demand will be sustained by a growing middle class that can afford high value-added products. The number of Chinese households with incomes over USD 35,000 is expected to rise to 160 million in 2030, from an estimated 48 million in 2020. At the same time the population is ageing, which will spur demand for drugs related to chronic illnesses.

We expect Indian pharmaceuticals output to grow by 1.8% in 2026 and by 12.7% in 2027. Most businesses have strong balance sheets and good access to bank financing. The government has introduced a National Pharmaceutical Policy (NPP), aimed at reducing drug costs and decreasing dependency on the import of Chinese active pharmaceutical ingredients (APIs). The policy offers financial incentives for the production of APIs, key starting materials and drug intermediates in India. As a result, India's API sector is expected to grow steadily, supporting the overall expansion of domestic pharmaceutical manufacturing. However, quality standard issues and incidents of alleged drug contamination remain downside risks.

India’s growing middle class and the increasing number of health insurance providers are enhancing access to medicines, which is expected to further stimulate domestic demand.

We expect pharmaceutical output in the ASEAN region to contract by 11.9% in 2026 after a whopping 16.8% surge last year. That said, we have observed significant sales growth of GLP-1 weight loss drugs in the first half of this year, in particular in Malaysia, Thailand and the Philippines. In 2027 pharmaceuticals output growth of 11.1% is expected, and the long-term growth prospects are favourable. Key drivers include rising middle-class incomes, healthcare system development, and increasing growth from both domestic and foreign investment. Despite global trade and pricing pressures, in general the credit risk of pharmaceutical businesses in Southeast Asia remains favourable with stable macroeconomic conditions.

Despite global trade and pricing pressures, the credit risk of pharma businesses in Southeast Asia remains favourable.

Pharmaceutical output is expected to grow by 3.9% in 2026 and by 5.8% in 2027, with generic drugs driving growth. The outlook for the market is promising, underpinned by government efforts to strengthen domestic manufacturing and enhance regulatory standards. Preferential procurement policies, targeted tax incentives and infrastructure investments are designed to reduce reliance on imports. However, price controls and mandatory public procurement discounts could limit margins and curb opportunities for innovative, patented medicines.

After growing 23.6% last year mainly due to front-loading activity in anticipation of US tariffs, we expect pharmaceutical production to contract by 18.0% this year. Washington’s announcement of additional US import tariffs in April 2026 will hurt the industry, as the Singapore is one of the top exporters of pharmaceutical products to the US. It exports predominantly expensive, patented drugs, and the country is not covered under any country-specific trade agreement. Singapore's tariff rate will jump from nearly 5% to almost 20%. That said, sector performance is supported by a business-friendly environment and proximity to key export markets in Asia. The credit risk situation of the industry remains very good. Singapore hosts regional headquarters for eight of the top 10 major pharmaceutical companies. There will be significant investments in new manufacturing sites by large foreign pharma businesses in the coming years.

Pharmaceutical production is expected to increase 1.1% this year after growing 5.2% in 2025. Sector performance is supported by universal healthcare, an ageing population and growing demand for chronic disease treatments. The country has a well-established domestic manufacturing base, with over 170 pharmaceutical manufacturers, most of which focus primarily on the production of generic drugs. In the coming years the sector will prioritise higher-value generics and biosimilars. Together with strengthened regulatory standards this should enhance competitiveness.

Pharmaceutical production is expected to contract by 5.7% this year, but to rebound strongly by 10.1% in 2027. The expansion of universal health coverage and economic growth will continue to stimulate the market. Along with plans to expand local pharmaceutical production, healthcare spending will rise further in the coming years, while global pharmaceutical businesses will increasingly seize the potential of Vietnam’s market. However, low levels of intellectual property protection could undermine investment prospects.

After sharply increasing by 14.6% in 2025, pharmaceuticals production in Western Europe is expected to contract by 2.7% in 2026, at least temporarily. The surge seen last year was due to front-loading triggered by massive US tariff threats, in particular benefitting Ireland. This year’s decrease reflects a correction from elevated production levels, but also softer external demand. Germany, Ireland, and Switzerland are expected to see production declines, while Denmark (up 6.5%) is a notable exception, supported by obesity-drug production.

US tariffs on EU patented drugs remain capped at 15%, and there are exemptions granted to individual European pharma companies that have agreed to increase their production processes in the US. This limits the impact of tariffs on the sector in the EU.

However, the effects of the Gulf conflict have affected industry performance due to higher oil and gas prices, some supply-chain disruptions and rising transport costs. All of this has fed straight into higher production and distribution costs for pharmaceuticals. Raw materials got noticeably more expensive, with most APIs and chemicals up 20–30%, and costs for some items like glycerine about 60% higher. On top of that, higher import prices, delays, and the need for bigger inventories have all added further pressure, pushing production costs up and squeezing margins for pharmaceutical firms across Europe. Generic drug makers, as well as contract development and manufacturing organisation (CDMO) businesses have experienced the most severe margin pressures, as they often operate energy-intensive facilities and cannot easily pass on costs under Europe’s drug pricing regulations. By contrast, large pharmaceutical companies (with diversified pipelines and stronger pricing power) have more capacity to absorb cost spikes, and so far remain less affected.

Higher energy and raw material prices and the need for bigger inventories are squeezing margins.

Even with the opening of the Strait of Hormuz the negative effects mentioned above will last into the second half of 2026, as the resume of traffic will be gradual. At the same time the downside risk of a re-escalation remains, which would have a serious impact on the credit risk of European pharmaceutical businesses.

The demand outlook for pharmaceuticals in Europe is solid in both the mid and long-term. Pharmaceuticals producers and wholesalers will benefit from the region’s ageing population, which will lead to increased demand for products to treat chronic illnesses and other conditions associated with ageing. However, most of the individual markets in Europe are highly regulated and many feature constraints that could impact pharma profits. There is permanent pressure from national health authorities to lower prices of drugs and medicines.

For the most part, financial indicators in the industry are structurally strong, but some SMEs could face financing challenges. This is due to high R&D costs, competition from India and China, and difficulty accessing financing at competitive interest rates. M&A activity between larger pharmaceutical producers and smaller, often specialist pharmas and biotech businesses is booming, and we expect this dynamic trend to continue in the coming years.

Looking ahead, European businesses face competitive disadvantages as more pharmaceutical businesses invest in the US and China, at the expense of investments in Europe. Despite well-established manufacturing facilities, secure supply chains and high production standards, the EU is facing gradually decreasing competitiveness in innovation. This is due to slower clinical trial setup times, weakening the ability to develop and produce new drugs early, in addition to less favourable regulatory and funding environments, and smaller patient pools compared to the US and China. The squeeze on the European pharmaceutical sector can be seen in the predicted compound annual growth rates (CAGR) for the world’s major manufacturing regions. 2025-2030 forecasts indicate CAGR for China pharma investments at 4.5%, the US at 3.0% and the EU and UK at 2.2%.

Download the full report in the related documents section below for a detailed analysis of the challenges, performance, and credit risks facing the pharmaceuticals industry’s major markets throughout the world.

To explore to strengthen your own credit risk strategy, get in touch with us and see how we can help you stay ahead.